Grantor Trust Versus Irrevocable Trust: Key 2025 Insights

You’re going to die. Sorry, but someone had to say it. Now, do you want your family to fight over your stuff in a glorious, never-ending death match, or do you want to actually understand what a grantor trust is before it’s too late? If you get these details wrong, you might as well toss your legacy, your tax savings, and your control out the window.

This article will give you the latest on grantor trust versus irrevocable trust for 2025 estate planning, so you can stop procrastinating and start making smart choices. We’ll cover what each trust is, how taxes work, who really owns your stuff, which trust keeps creditors at bay, what’s changed in the law, and some real-world examples. Read on if you want to avoid costly mistakes and finally get your estate plan together.

Understanding Grantor Trusts in 2025

Congratulations, you’ve made it to the part of adulthood where “grantor trust” sounds less like a monster under the bed and more like the monster hiding in your estate plan. If you think trusts are only for billionaires and Bond villains, think again. In 2025, knowing what a grantor trust is (and isn’t) could make the difference between your heirs getting your hard-earned cash or your least favorite relative getting your vintage PlayStation. Let’s break down what makes a grantor trust tick, why the IRS cares, and how you can use it to keep your legacy from becoming a family wrestling match.

Definition and Core Features

A grantor trust is not some secret handshake or a password to an exclusive club — it’s a legal structure where you, the grantor, keep enough control that the IRS basically says, “Nice try, but we still see you.”

Here’s what typically counts as control:

- Power to revoke or amend the trust whenever you get bored

- Ability to swap out trust assets like you’re trading baseball cards

- Directing how, when, and to whom the trust makes distributions

Most revocable living trusts are grantor trusts by default, but even some irrevocable trusts can sneak in under the grantor trust label if you retain the right powers.

For tax purposes, the grantor trust is a “disregarded entity,” which sounds cool but really means the IRS pretends the trust doesn’t exist — they tax you directly. According to 2025 IRS guidelines, the thresholds for income and estate inclusion haven’t gotten any friendlier.

Example: You set up a revocable living trust, keep managing your investments, and decide when your kids get their inheritance. Spoiler: You’re still in the driver’s seat, for better or worse.

Bottom line: The grantor trust is the Swiss Army knife of estate planning — flexible, sharp, and a little dangerous in the wrong hands.

Taxation of Grantor Trusts

Here’s where the grantor trust starts to feel like both a superpower and a mild curse. All income the trust earns? Yeah, that’s on your personal tax return. No separate tax ID needed, just you and your favorite IRS forms bonding over dividends and capital gains.

Let’s get real about tax brackets:

- Trusts hit the top 37% rate at $15,650 in 2025

- Individuals don’t get there until $626,351

But since the grantor trust is ignored for tax purposes, you get to use your personal (usually lower) rates. That can mean big savings, especially if your trust is raking in serious investment income.

However, every asset in a grantor trust is still part of your estate for estate tax. If you’re aiming for tax ninja moves, the Intentionally Defective Grantor Trust (IDGT) is a classic: you can sell assets to your own trust without triggering capital gains. It’s not cheating — it’s just creative adulting.

Example: You sell an appreciated property to your IDGT, get a promissory note, and avoid immediate capital gains tax.

Worried about the IRS closing loopholes? You’re not alone. The Grantor Trusts Rules: Will Loopholes Be Closed in 2025? article is worth a read if you want to keep your estate plan ahead of the legislative curve.

When and Why to Use a Grantor Trust

Let’s face it, you want control. A grantor trust lets you keep your hands firmly on the wheel while you’re alive. Pay the taxes yourself, let the trust assets grow faster, and set up rules for how your money gets handed down — all without giving up the keys.

Common uses:

- Grantor Retained Annuity Trusts (GRATs) for squeezing more out of your estate

- Spousal Lifetime Access Trusts (SLATs) to provide for your beloved (or barely tolerated) spouse

- Irrevocable Life Insurance Trusts (ILITs) for sheltering life insurance from estate taxes

Setting up a grantor trust isn’t rocket science, but get a pro — either a sharp attorney or estate planning software with a pulse. Pros: flexibility, tax advantages, peace of mind that your heir won’t spend your fortune on NFTs. Cons: assets are still in your estate, and you get stuck with the tax bill every year.

Example: You use a grantor trust to provide income to your spouse while minimizing gift tax exposure, all while keeping your ex from sniffing around your assets.

The grantor trust is tailor-made for anyone craving control and tax leverage. But remember, with great power comes great responsibility — and possibly a bigger tax bill.

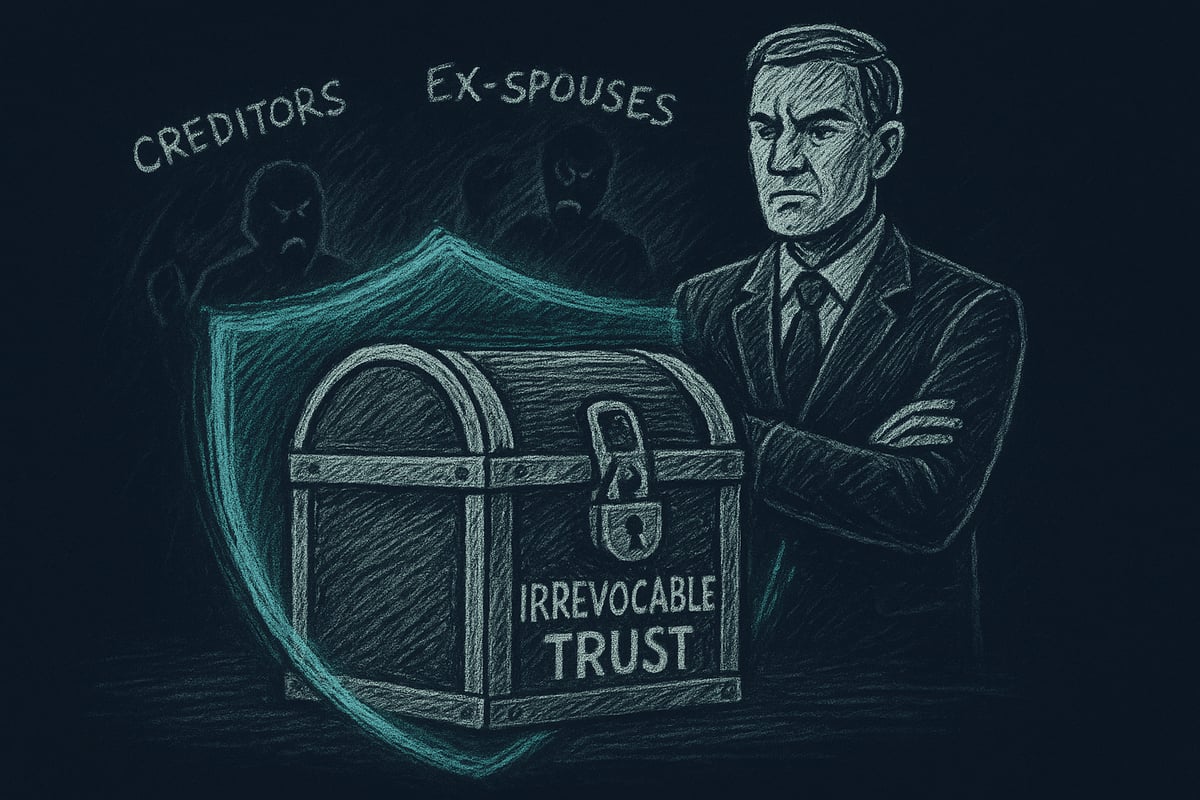

Irrevocable Trusts: Structure and Strategy

So, you finally realized stuffing cash under your mattress will not keep your ex from raiding your life’s savings. Welcome to the world of irrevocable trusts, where you give up control now to prevent a family feud later. The main difference between an irrevocable trust and a grantor trust? Once you set up an irrevocable trust, you are not the boss anymore. The assets are gone from your estate, and a trustee calls the shots. Let us see why that is sometimes exactly what you need.

What Makes a Trust Irrevocable?

Picture this: You set up a trust, hand over the keys, and then—surprise—you cannot change your mind. That is the magic (or curse) of an irrevocable trust. You, the grantor, toss control out the window. The trustee must run the show according to the trust document, not your whims.

Common types include bypass trusts, charitable remainder trusts (CRTs), qualified personal residence trusts (QPRTs), and dynasty trusts. For example, an irrevocable life insurance trust (ILIT) shelters life insurance proceeds from estate tax, which is a neat trick if you do not want Uncle Sam getting the last laugh.

Asset protection is a big draw—creditors and lawsuit-happy exes cannot touch what is inside. If you are still on the fence about control versus protection, check out this Revocable vs Irrevocable Trusts: Control vs Protection guide for a reality check.

Irrevocable trusts are not for the faint of heart. But if you want ironclad asset protection and estate tax minimization, they are the gold standard.

Taxation of Irrevocable Trusts in 2025

Get ready for some tax fun. Unlike a grantor trust, an irrevocable trust is its own legal entity. It files Form 1041 and gets a TIN, just like your least favorite corporation. Income kept in the trust is taxed at trust rates, which skyrocket fast—37 percent at just $15,650 in 2025. If the trust pays out income, beneficiaries get a K-1 and the tax bill.

Do not forget the Net Investment Income Tax (NIIT)—a 3.8 percent kicker on trust income above $14,450. The upside? Assets and all future appreciation are kicked out of your estate, side-stepping estate tax. Funding an irrevocable trust is a classic move to “freeze” asset values and keep the IRS guessing.

Gift tax is the catch: Transfers into the trust may eat up your $13.99 million lifetime exemption, but hey, that is what it is there for. And thanks to the OBBA Act, non-grantor trusts can grab a $40,000 SALT deduction in 2025, making your accountant less grumpy.

When and Why to Use an Irrevocable Trust

Why bother with all this irreversible drama? Because sometimes, the only way to protect your assets from creditors, lawsuits, or your kid’s future ex is to put them out of reach. Irrevocable trusts are perfect for high-flyers who want to move appreciating assets out of their estate, slice estate taxes, or provide for heirs who might burn through cash faster than lottery winners.

They are also great for charitable giving via CRTs and CLTs or for setting up special needs or spendthrift protections. The tradeoff? You lose control. Once the ink dries, changes are nearly impossible. Setting up an irrevocable trust requires serious legal muscle and a willingness to let go—no take-backs.

Let us say you use a QPRT to pass your house to your kids at a reduced gift tax value. You get to live there for a while, then—poof—it is theirs, and you have kept the IRS at bay.

In short, if you want to shield wealth, minimize taxes, and do not mind surrendering control, this is your ticket. But if you crave flexibility, a grantor trust might fit better. Either way, your future self (and your heirs) will thank you—probably.

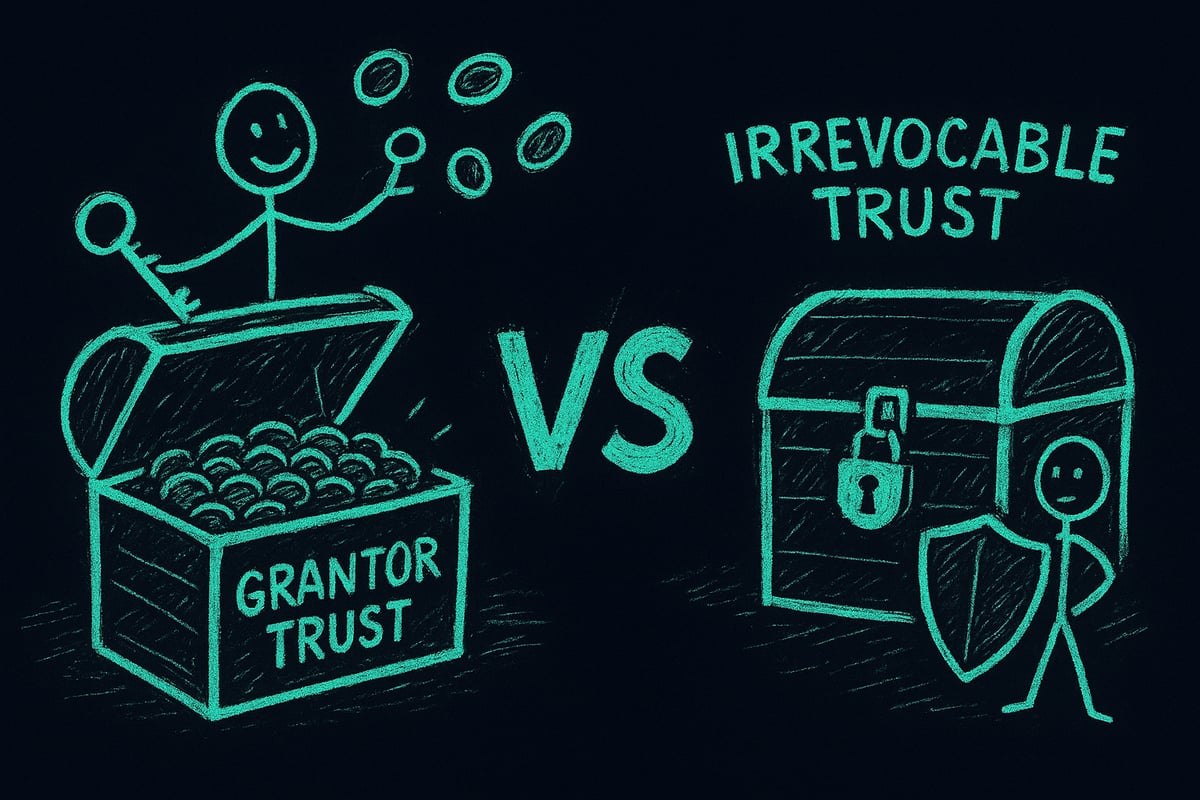

Grantor Trust vs. Irrevocable Trust: Key Differences

Ever wondered if your “death party” will come with a side of family lawsuits or surprise taxes? Let’s break down the real-life drama between a grantor trust and an irrevocable trust. Spoiler: One gives you control, the other gives your creditors the finger. Ready for the main event?

Control and Flexibility

With a grantor trust, you’re still the captain of your own ship. You can amend, revoke, or micromanage assets whenever the mood strikes. Think of it as a “choose your own adventure” for your estate plan. Want to swap out investments or change who gets your stuff? Go for it. You hold the power, and the pen.

Irrevocable trusts, on the other hand, are like putting your assets in a vault and giving someone else the combination. Once you set it up, you can’t touch the controls. The trustee calls the shots, and your meddling days are over. Beneficiary changes? Not happening.

Here’s a quick table if you’re already skimming:

| Feature | Grantor Trust | Irrevocable Trust |

|---|---|---|

| Can change terms | Yes | No |

| Control assets | Yes | No |

| Trustee powers | Usually you | Independent party |

Bottom line: More control with a grantor trust, but less protection. Want to rule from the grave? Sorry, only if you pick wisely.

Taxation and Estate Inclusion

Here’s where things get spicy. With a grantor trust, all the trust’s income waltzes onto your personal tax return. No separate tax ID, no hiding from the IRS. You get the privilege of paying taxes on every dollar, even if you never touch the cash. Bonus: the assets are still part of your estate when you take your final bow.

Irrevocable trusts are different. They file their own return (Form 1041), snag their own TIN, and pay taxes at trust rates unless they distribute income to beneficiaries. And trust tax rates? They get brutal, hitting 37 percent at just $15,650 in 2025. Compare that to your personal bracket, which doesn’t hit that high until you’re rolling in over $626,351. If you want to get clever with state taxes, check out strategies like New SALT Cap Deduction: Tax Savings with Non-Grantor Trusts for an extra layer of fun.

Trusts also face a 3.8 percent Net Investment Income Tax above $14,450. So, if you’re thinking of stuffing assets into an irrevocable trust to “freeze” their value for estate taxes, congrats—you’re only slightly less irresponsible than you were ten minutes ago.

The key takeaway: Grantor trust means you pay taxes now and later, while irrevocable trust shifts the pain to the trust or your heirs. Choose your headache.

Asset Protection and Creditor Exposure

Let’s talk about your creditors and that ex who still wants your PlayStation. If your assets are in a grantor trust, guess what? Your creditors can still reach in and grab them. It’s like locking your door but leaving the window open.

Irrevocable trusts, though, are the fortress you wish you had in college. Assets are shielded from most lawsuits, divorces, and creditors. State law does play a role, so pick your trustee and trust location with care—some places are friendlier than others.

Picture this: You use a grantor trust, and your kid’s inheritance is up for grabs in their next messy divorce. Oops. Use an irrevocable trust, and suddenly, your ex-son-in-law is out of luck.

In short: If you want real protection, an irrevocable trust is your best bet. With a grantor trust, you get flexibility, but your assets stay exposed. Don’t say I didn’t warn you.

2025 Legal and Tax Updates Impacting Trust Planning

You know what’s scarier than your own mortality? The IRS. If you think your estate plan is “done” because you scribbled your will on a napkin in 2022, think again. The rules around grantor trust and irrevocable trust planning are changing in 2025, and the government is not sending you a reminder text. Here’s what you need to know before your procrastination becomes your family’s problem.

Recent Legislative Changes (ATRA, OBBA, TCJA)

Congress, in its infinite wisdom, keeps moving the estate planning goalposts. The American Taxpayer Relief Act (ATRA), the One Big Beautiful Bill Act (OBBA), and the Tax Cuts and Jobs Act (TCJA) have all dropped fresh wrinkles into the trust game. The estate tax exemption is $13.99 million for 2025, jumping to $15 million in 2026. If you blink, you might miss your chance to shelter assets for your heirs.

OBBA now lets each non-grantor trust deduct up to $40,000 in state and local taxes (SALT) per year from 2025 through 2029. The Net Investment Income Tax (NIIT) slaps a 3.8% toll on trust income above $14,450. Translation: fewer folks will pay federal estate tax, but the income tax squeeze is real.

We’re seeing a shift—many now consider whether an irrevocable grantor trust is the answer in 2025, and if you want to dive deeper, check out Are Irrevocable Grantor Trusts the Answer in 2025?. It’s proof that even lawyers get nervous about the future.

Managing State Income Tax for Trusts

State tax law: because the IRS wasn’t complicated enough. Each state has its own “logic” for taxing trusts. Some look at where the trustee lives, others at the grantor’s last known zip code, and a few just want a cut of anything that moves. For example, Oregon will take 9.9% of your trust’s income, while Nevada politely takes nothing.

If you set up a grantor trust, your home state will tax you, no matter where your trustee is. Non-grantor trusts, though, can shift state tax liability—choose your trustee’s location wisely, or you’ll end up funding a state’s road repair budget. Picture this: a Nevada resident picks an Oregon trustee, and suddenly Oregon’s got a hand in the cookie jar.

Bottom line: strategic planning for trust situs and trustee selection is not “extra credit”—it’s crucial for keeping your estate plan from turning into a tax piñata.

Practical Scenarios and Case Studies

Let’s get real. Here’s how these updates play out in the wild:

- Scenario 1: Use a grantor trust to move assets to kids, keep control, and enjoy flexible distributions—until you decide you actually hate taxes.

- Scenario 2: Lock up your wealth in an irrevocable trust, protecting it from creditors and your ex, while minimizing estate taxes.

- Scenario 3: Change your mind? Convert a grantor trust to non-grantor as your wealth grows or laws shift.

- Scenario 4: Create multiple non-grantor trusts to maximize those sweet, sweet SALT deductions.

Every choice is a tradeoff: control versus protection, tax now or tax later, flexibility or finality. There’s no one-size-fits-all. The only real mistake? Not planning at all.

Choosing the Right Trust for Your Estate Plan

So, you’ve finally decided to stop tempting fate and actually plan for the inevitable. Good for you. Now, the real fun begins: picking the right trust. Do you want your family to inherit your hard-earned cash, or do you want your ex to buy a jet ski with it? The choice is yours, but only if you choose wisely. Let’s break down what matters in 2025.

Factors to Consider in 2025

Stop me if you’ve heard this one before: someone sets up a grantor trust thinking it’s a silver bullet, only to discover their assets are about as protected as a sandwich at a seagull convention. Before you leap, ask yourself:

- How much control do you need? Do you want to micromanage from the grave, or are you cool letting go?

- What are your asset types? Real estate, business, crypto, or just a collection of questionable art?

- Family dynamics: Got a spendthrift heir, a special needs child, or a future ex-spouse to plan around?

- Tax implications: Are you trying to dodge the IRS or just minimize the pain?

- Flexibility: Can your trust adapt as laws and your life change, or is it set in stone?

- Professional guidance: Spoiler alert, DIY is not the move here.

Here’s a quick look at how a grantor trust stacks up:

| Feature | Grantor Trust | Irrevocable Trust |

|---|---|---|

| Control | High | Low |

| Asset Protection | Low | High |

| Estate Inclusion | Yes | No |

| Tax Complexity | Moderate | High |

If your family’s wealth is mostly tied up in real estate, a grantor trust with QPRT provisions could be your ticket. Entrepreneurs? Check out IDGTs for tax leverage. Want to keep your legacy from becoming a family feud? Get professional help, fast.

Common Mistakes and How to Avoid Them

Let’s be honest, most people mess this up. Don’t be most people. Watch out for these classic blunders:

- Forgetting about state tax rules and residency quirks.

- Picking the wrong trust for your family’s actual needs.

- Ignoring how fast trust tax brackets max out (trusts hit 37 percent at $15,650 in 2025).

- Letting your trust gather dust as laws and your life shift.

- Underestimating how little control you’ll have with an irrevocable trust.

- Accidentally keeping powers in a grantor trust that drag assets back into your estate.

Trusts aren’t set-it-and-forget-it. Regular reviews and honest conversations with pros can save your heirs from a bureaucratic nightmare.

Professional Tools and Resources for Estate Planning

Ready to do this right? Here’s what you actually need:

- Estate planning attorney: The only person more paranoid about your death than you.

- Fiduciary software: Because Excel is for grocery lists, not legacies.

- Tax calculators: Handle those compressed brackets before they handle you.

- Up-to-date documents: Old wills are about as useful as expired milk.

- Financial advisors: They see the big picture, even if you don’t.

- Checklists and guides: The IRS has plenty, but try not to fall asleep reading them. Start with IRS Estate Planning Resources.

Fun fact: Over 3,000 advisors use digital platforms to make sure your grantor trust isn’t a ticking time bomb. Don’t be the one person who trusts sticky notes over professionals.

No two estate plans look the same in 2025, and that’s a good thing. The right tools and advice will keep your money where it belongs: out of probate court and away from your ex’s new speedboat.

Look, you just waded through the difference between grantor and irrevocable trusts—so you’re already doing better than 95% of people who think “estate planning” means picking out a tombstone font. The truth is, you’re going to die. Your family shouldn’t have to fight over your stuff when you do, or get ambushed by taxes and legal headaches. Why not lock down your legacy now and save them from the world’s most awkward family reunion? It takes less time than bingeing one episode, and you don’t need a law degree or a pile of cash.

Start My Will Now