Guide to Statutory Durable Power of Attorney: 2025 Update

Think you’re invincible? That’s adorable. Life has a funny way of proving otherwise, usually at the worst possible moment. Enter the statutory durable power of attorney, your last line of defense when you can’t defend yourself—or your bank account.

This guide is your no-nonsense roadmap to what the statutory durable power of attorney actually is, why it matters in 2025, and how it keeps your finances safe from chaos (and your relatives’ bad decisions).

We’ll break down legal must-knows, new 2025 updates, practical steps, and those classic mistakes everyone makes. Want to protect your money and your choices? Get ready to take action and finally stop putting this off.

What is a Statutory Durable Power of Attorney?

So, what exactly is a statutory durable power of attorney? Think of it as the legal equivalent of designating a financial stunt double. This document lets you, the principal, hand over control of your money and property to an agent you trust. Unlike a medical power of attorney, the statutory durable power of attorney does not let your agent make healthcare decisions. Its “durable” superpower means it sticks around even if you’re knocked out of commission. Imagine you’re in a coma—your agent can still pay your bills and manage your investments. Without this backbone of financial continuity, your money could end up gathering dust while your family argues about who gets to pay the electric bill. If you want a play-by-play on how these forms work, check out the Texas Statutory Durable Power of Attorney Form Guide.

Definition and Distinction from Other POAs

A statutory durable power of attorney is a legal document that hands your financial and property decisions to a chosen agent. Unlike a medical POA, which covers only healthcare choices, the statutory durable power of attorney sticks to the money side of things. The “durable” part means it keeps working if you lose mental capacity. Picture this: you’re out cold, but someone still needs to pay the mortgage and handle your investments. That’s where your agent steps in. Without this, your family could be stuck waiting for a court order just to keep the lights on. In short, the statutory durable power of attorney is the unsung hero of your financial survival kit.

Why SDPOA Matters in 2025

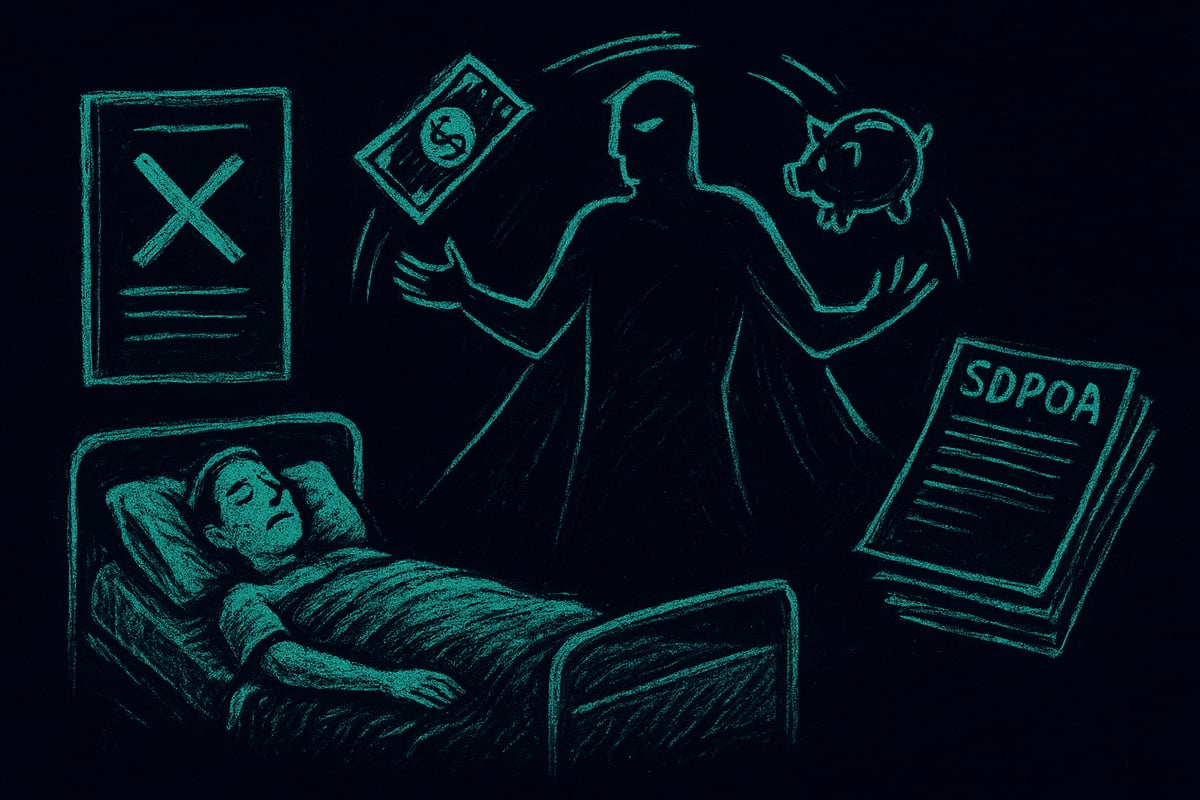

Let’s face it, you’re not immortal. With more people living longer and surprise illnesses lurking around every corner, incapacity is a real threat. Here’s the reality check: about 70 percent of adults die without a will or power of attorney, leaving loved ones tangled in legal chaos. Financial institutions are playing hardball, too—they often refuse access to accounts without the magic words “statutory durable power of attorney.” Imagine your adult kids unable to touch your funds when you need care. Probate delays and costs skyrocket if you don’t have this in place. In 2025, not having a statutory durable power of attorney is practically an invitation for disaster.

Powers Granted and Limitations

What can an agent do with a statutory durable power of attorney? A lot, but not everything. Typical powers include managing bank accounts, selling real estate, handling investments, and dealing with taxes. You can customize what your agent can and can’t do, keeping things broad or laser-focused. But don’t get cocky—your agent can’t write or change your will, and they can’t touch your medical decisions. For example, a statutory durable power of attorney could let your agent sell your home to pay for elder care, but not decide on your surgery. Its flexibility is a blessing and a risk, so choose wisely.

Legal Requirements and 2025 Updates

So, you finally decided to get your statutory durable power of attorney in order Congratulations on being less reckless than your neighbor But hold on not all SDPOAs are created equal If you want your family to avoid a bureaucratic nightmare, you need to get the details right Let s dissect exactly what it takes to make your statutory durable power of attorney bulletproof in 2025

Core Legal Requirements for Valid SDPOA

First rule of surviving incapacity: your statutory durable power of attorney must actually be valid That means the person signing (the principal) must have their mental marbles at the time No, your drunk uncle s signature at Thanksgiving does not count

The form itself has to play by your state s rules—think Texas Estates Code, or whatever your flavor of bureaucracy is And yes, notarization is usually a must Skip it, and watch your bank laugh you out the door

Here s a quick comparison for the overachievers:

| Requirement | Statutory Form | Custom-Drafted Form |

|---|---|---|

| State Compliance | Guaranteed | Must be verified |

| Notarization | Required | Required |

| Flexibility | Limited | High |

If you hand in an unnotarized statutory durable power of attorney, expect your bank to shut you down faster than your last Tinder date

2025 Legislative Changes and Their Impact

Welcome to 2025, where your statutory durable power of attorney can finally be digital—yes, your printer can rest Now, digital and photocopied SDPOAs are gaining legal acceptance in most states Co-agents can act solo unless you specifically say they can t Financial institutions are now legally required to stop dragging their feet and honor valid SDPOAs, or else face real consequences

Agents are also under the microscope more than ever, with new accountability rules Picture this: you email a digital SDPOA for a real estate closing, and it s accepted Progress For a deep dive into these changes, check out 2024/2025 Legislative Updates on Estate Planning if you want to impress your lawyer friends

Bottom line The 2025 landscape for statutory durable power of attorney is more digital, more flexible, and a lot less forgiving of sloppiness

State-by-State Variations and Compliance

Spoiler alert: your statutory durable power of attorney is not a universal skeleton key Each state has its own form, its own quirks, and its own way of making your life harder Using a 2024 form in 2025 is like showing up to a costume party in last year s meme—cringe and possibly rejected

Move to another state Your old Texas SDPOA will not charm the banks in California Always update your statutory durable power of attorney when you relocate or if your state updates its statutes

Legal compliance is not just a suggestion, it s your shield against future headaches You don t want your family fighting over your Netflix password, let alone your house

Common Mistakes and How to Avoid Them

Let s roast some classic mistakes People love to hand over broad powers in their statutory durable power of attorney without thinking Or they forget to update after a divorce, new job, or the latest season of existential dread

Top errors to dodge:

- Fuzzy or vague powers

- Outdated forms (2023 called, it wants its SDPOA back)

- Forgetting to tell your bank or broker about the new document

Imagine needing urgent access to funds, only to watch your statutory durable power of attorney get rejected because it was drafted during the Paleozoic era Pro tip: stay current, stay clear, and tell the right people

Step-by-Step Guide to Setting Up a Statutory Durable Power of Attorney

Congratulations, you’ve decided to adult for a moment and face your own mortality. Setting up a statutory durable power of attorney doesn’t require a séance, just some common sense and a few signatures. Here’s your step-by-step guide to making sure your assets don’t end up in probate purgatory.

Step 1: Assess Your Needs and Choose Your Agent

First, take a cold, hard look at your finances. What needs protection if you’re suddenly out of commission—your bank accounts, investments, or that collection of rare Beanie Babies? The statutory durable power of attorney lets you choose who gets to call the shots when you can’t.

Make a list of potential agents. Pick someone trustworthy, financially literate, and unlikely to run off to Vegas with your life savings. Think about naming a backup agent, because life happens and sometimes your first pick is busy binge-watching legal dramas.

Agent Criteria Table:

| Criteria | Why It Matters |

|---|---|

| Trustworthiness | No embezzlers, please |

| Financial know-how | Can balance a checkbook |

| No conflicts of interest | Won’t buy your car for $1 |

Example: Choosing your CPA sibling over your flaky cousin is a win. Don’t give the keys to your kingdom to someone who thinks “fiduciary” is a new TikTok dance.

Step 2: Drafting and Customizing Your SDPOA

Now, grab your state’s latest statutory durable power of attorney form. Don’t use that dusty template from 2009—laws change, and so do your options. In Texas, for example, recent changes give agents new powers and responsibilities, so double-check you’re using the 2025 version.

Decide if you want your agent to handle everything or just specific tasks. You can limit authority to, say, selling your house but not touching your crypto wallet. Add clear instructions if you want to restrict or clarify powers. Overly broad authority is like handing someone a blank check—don’t do it unless you’re cool with surprises.

Example: You might limit your agent’s power to real estate transactions only if you don’t want them dabbling in your other assets. Be precise. Vague instructions lead to chaos, and chaos is expensive.

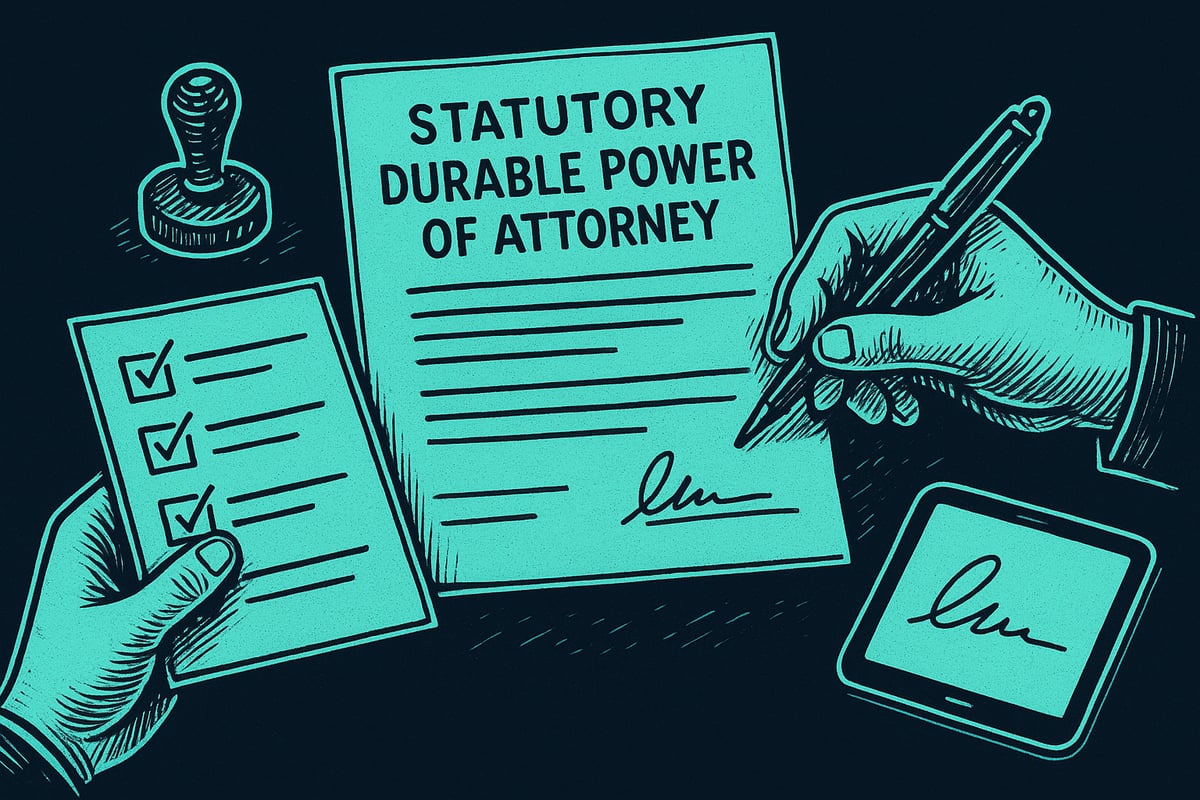

Step 3: Executing the Document Properly

Ready to make it official? Sign your statutory durable power of attorney in front of a notary. Some states want witnesses too, so check your local rules. You must be of sound mind—no, being halfway through a bottle of wine doesn’t count.

Once signed, stash the original somewhere safe but accessible. Forgetting where you put it is a classic move. If your agent can’t get the document in an emergency, your planning is pointless.

Pro tip: Give copies to your agent and key financial institutions. If you lock it in a safe deposit box, make sure your agent can actually open it. Otherwise, your “plan” will be as effective as hiding your will in the freezer.

Step 4: Notifying Third Parties and Ensuring Acceptance

Don’t wait for a crisis to tell your bank about your statutory durable power of attorney. Notify every relevant institution—banks, investment firms, mortgage companies—before disaster strikes. Submit copies in advance and confirm they’ll honor it.

Sometimes, financial institutions act like you’re handing them a forged treasure map. If a bank refuses your SDPOA, escalate politely and remind them of your rights. The 2025 laws are on your side, so don’t let bureaucratic nonsense derail your plan.

Being proactive now means your agent won’t be stuck in red tape when you need help most. Remember, the statutory durable power of attorney only works if the right people know it exists.

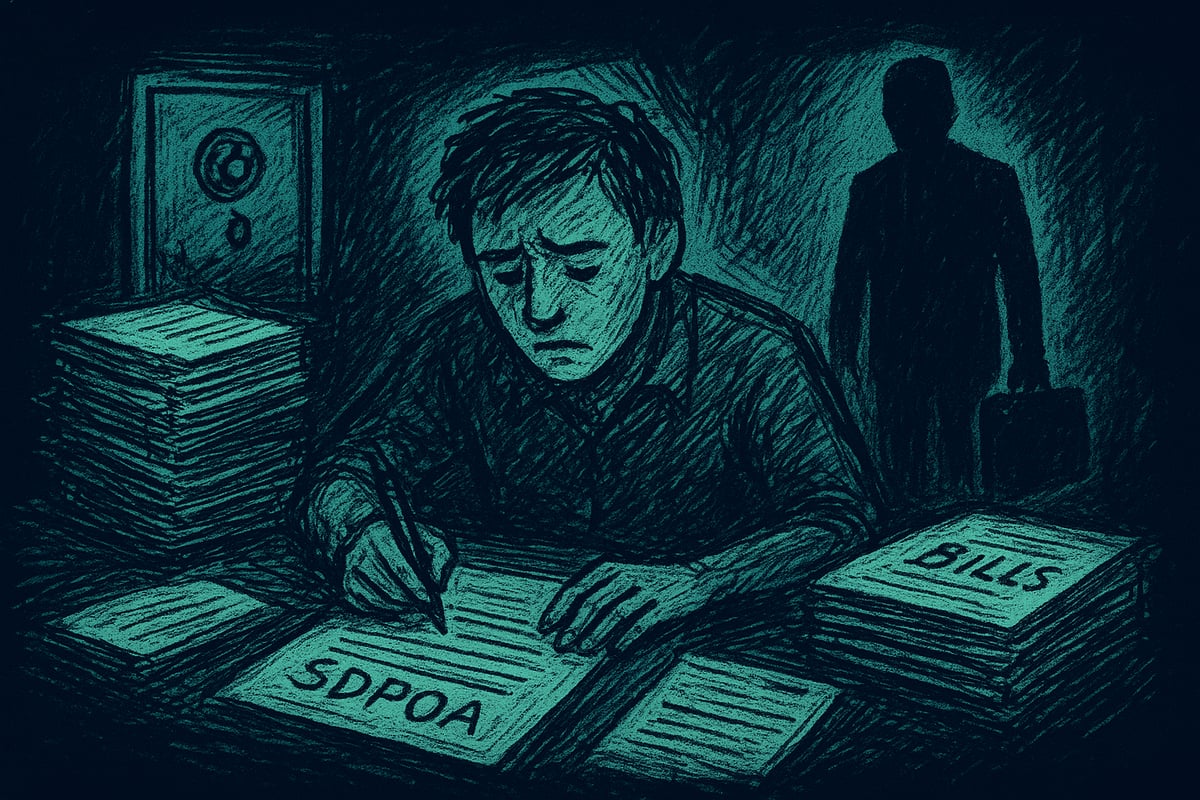

Agent Responsibilities and Accountability

You picked someone to boss your money around with a statutory durable power of attorney? Congratulations, you’re officially trusting another human with your financial life. What could possibly go wrong? Let’s break down exactly what your agent can and can’t pull off, and how you can keep them from turning your legacy into their personal shopping spree.

Scope of Agent’s Authority and Fiduciary Duty

When you hand someone a statutory durable power of attorney, you’re giving them the keys to your financial kingdom. This doesn’t mean they get to buy a Ferrari in your name (unless you’re into that). The agent’s authority is strictly limited to what you’ve spelled out. They can pay your bills, manage your investments, or sell your house, but only if you said so.

Here’s the catch: every agent has a fiduciary duty. That’s legal speak for “don’t be shady.” They must act in your best interests, keep records, and avoid mixing your money with theirs. If they treat your checking account like a piggy bank, they’re in for a world of legal hurt. For a state-specific look at what this really means, check out Durable Power of Attorney Essentials in Florida.

Failing to keep receipts or explain transactions? That’s a fast track to a courtroom drama your family didn’t ask for.

Oversight, Checks, and Balances

Let’s be honest: absolute power corrupts absolutely, even if your agent is “just your brother.” That’s why the statutory durable power of attorney allows for some oversight. You can appoint co-agents, so two people have to agree before any big moves, or require regular accounting to nosey relatives.

Pro tip: add a third-party watchdog, like your lawyer or a trusted friend, to review the agent’s activity. You can even demand periodic financial reports, because nothing says “I love you” like a little distrust. Regularly reviewing and updating your statutory durable power of attorney is the adult version of changing your Netflix password after a breakup.

If you want your agent to stay honest, make sure someone is watching. It’s not paranoia, it’s just smart estate planning.

Revoking or Amending an SDPOA

Changed your mind? Decided your agent is less Warren Buffet and more Bernie Madoff? Good news: as long as you’re mentally competent, you can yank that statutory durable power of attorney faster than you can say “never mind.” Just draft a written revocation, sign it, and hand it out to every bank, broker, and nosy neighbor who got a copy of the original.

Updating your statutory durable power of attorney is crucial after major life events: divorce, moving states, or finally realizing your ex doesn’t deserve access to your crypto wallet. If you don’t notify everyone, chaos will follow. Picture your ex draining your account while your new spouse is left arguing with bank clerks. Not a good look.

Stay in control, keep everyone in the loop, and don’t assume your agent is a saint just because they share your DNA.

Frequently Asked Questions About SDPOA

Got burning questions about the statutory durable power of attorney? Good. If you’re thinking, “Wait, do I really need to care about this?”—the answer is yes. Let’s roast your procrastination and clear up the fog, one awkward question at a time.

Can I Appoint Multiple Agents?

Absolutely, you can appoint multiple agents under your statutory durable power of attorney. You can make them act jointly or let them run wild independently—your circus, your monkeys.

- Joint agents must agree on every move. This can be like herding cats.

- Independent agents can act solo, which means faster decisions but also more room for drama.

Example: Appoint your two kids. They can both pay your bills, but if they hate each other, expect fireworks.

Does SDPOA End at Death?

Yes, the statutory durable power of attorney dies with you. Sorry, your agent doesn’t get to keep playing Monopoly with your assets forever.

- When you shuffle off this mortal coil, the executor takes over.

- Your agent cannot access accounts or make decisions after your death.

Example: If your agent tries to dip into your account after you’re gone, the bank will shut that down fast.

How Do I Revoke or Update My SDPOA?

You can revoke your statutory durable power of attorney any time, as long as you’re still mentally competent. Just write a revocation, sign it, and send it to everyone who matters.

- Update after major life events like marriage, divorce, or moving to a new state.

- Don’t forget to actually tell your banks and agents about changes.

Example: You move to Florida. Update your SDPOA or risk your ex controlling your beach condo. Fun, right?

Is an Attorney Required to Create an SDPOA?

Nope, you don’t have to pay a lawyer to wield the mighty statutory durable power of attorney. There are state-approved forms for DIY types.

- If your estate is complicated, or you own a business, talk to a pro.

- Statutory forms are cheap, but mistakes aren’t.

Example: Blended family? Business in three states? Don’t be a hero—get legal help.

What Happens if I Don’t Have an SDPOA?

Brace yourself. No statutory durable power of attorney means your family gets a front-row seat to the legal Olympics: court-appointed guardianship.

- Frozen assets, legal fees, and endless paperwork await.

- Months can go by before anyone can pay your bills or care for you.

- For more on avoiding this nightmare, check out Nolo’s POA Guide.

Example: Your care bills pile up while your family squares off in court. Trust me, it’s uglier than a reality TV reunion.

Can I Use Digital or Photocopied SDPOAs?

Welcome to 2025. Digital and photocopied statutory durable power of attorney documents are now widely accepted, but check with each institution first.

- Some banks still cling to the past and want originals.

- Others are happy with a PDF and a handshake (okay, maybe just the PDF).

Example: Your scanned SDPOA gets you into your investment account, but your local bank wants to see paper. Be ready for both.

Recent Trends, Pitfalls, and Expert Tips for 2025

So, you think your statutory durable power of attorney is bulletproof? Let’s talk about what’s actually happening in 2025, because your old-school paper might be about as useful as a floppy disk.

Digital Platforms: The New (Annoying) Normal

In 2025, digital estate planning platforms are everywhere. Setting up a statutory durable power of attorney online is as easy as ordering takeout, but just as risky if you’re not paying attention. Some banks now accept digital or scanned SDPOAs, while others still act like it’s 1995 and demand an original with a wax seal. Don’t assume your digital document will magically work everywhere.

Pitfalls and How to Dodge Them

Let’s play everyone’s favorite game: “How Will My Family Get Stuck in Probate?” Here’s a cheat sheet to keep your statutory durable power of attorney from being an epic fail:

| Pitfall | Consequence | Solution |

|---|---|---|

| Outdated SDPOA | Rejected by institutions | Use 2025 forms, review annually |

| Not notifying banks | Delays in access | Proactively submit copies |

| Assuming it covers medical choices | Medical chaos | Get a separate Medical POA |

| No updates after life changes | Wrong people in charge | Update after marriage, divorce, move |

Only 30% of Americans even have a statutory durable power of attorney. The other 70%? They’re playing legal roulette, hoping their family can pay the bills when they’re out of commission. Don’t be that person.

Expert Tips for the Perpetually Distracted

- Review your statutory durable power of attorney every year. Yes, every year. Put it on your death party calendar.

- After any big life event (marriage, divorce, moving to another state), update your document.

- Test your SDPOA with your bank and investment firm now, not during a medical emergency.

- Don’t trust that one-size-fits-all forms have you covered. If your situation is weird (blended family, business, ex who still wants your PlayStation), talk to a pro. Here’s a reputable SDPOA resource for 2025 forms.

Congrats! You’re already ahead of the 70% who are still procrastinating. Remember, a statutory durable power of attorney isn’t just for the wealthy or the elderly. It’s for anyone who’d rather not have their family stuck in court, fighting over frozen assets while you’re out cold.

Look, you made it this far without falling asleep or running for the hills—impressive. The truth is, you’re not immortal, and your family shouldn’t have to host a courtroom drama just because you couldn’t be bothered to fill out a few forms. We’ve roasted the legal mumbo jumbo for you, sliced through the confusion, and given you the tools to dodge financial chaos when life goes sideways. So, why not take the extra step and make sure your will is sorted, too? Congrats! You’re about to be slightly less irresponsible. Start My Will Now

Related Articles You Should Read

What Happens If You Die Without a Will in Tennessee: 2026 Complete Guide

What Happens If You Die Without a Will in Tennessee: 2026 Complete Guide Meta Description: Dying without a will in Te...

What Happens If You Die Without a Will in Pennsylvania: 2026 Guide

What Happens If You Die Without a Will in Pennsylvania: 2026 Guide Meta Description: Die without a will in Pennsylvan...

What Happens If You Die Without a Will in New York: 2026 Complete Guide

What Happens If You Die Without a Will in New York: 2026 Complete Guide Meta Description: Die without a will in New Y...